Headline economics — base scenario

§ 01 · SCENARIO PACKFive scenarios, one verdict each.

Tier 1 ran one scenario. Tier 2 runs five — base plus four named stresses the IC has historically asked about. Each scenario is a full Monte Carlo on the selected stack; the table below summarizes whether each one clears the IRR hurdle.

| Scenario | NPV | IRR | LOLE | Verdict |

|---|---|---|---|---|

| base | +$11.8 M | 8.7% | 0.0 / yr | Pass |

| utility_slip_stress (+12 mo) | +$3.4 M | 8.1% | 0.0 / yr | Pass · margin compressed |

| tariff_stress (post-rider y11+) | +$10.4 M | 8.5% | 0.0 / yr | Pass |

| capex_stress (+15%) | +$3.4 M | 8.0% | 0.0 / yr | Pass at floor |

| stretch_upside (-6 mo) | +$15.6 M | 9.4% | 0.0 / yr | Pass with upside |

The project clears the hurdle in five out of five scenarios. The binding stress is capex_stress at 8.0% IRR — exactly at the hurdle. That's the headline finding: the project survives a 12-month utility slip and survives a post-rider tariff rise, but a +15% capex shift leaves no margin. Procurement discipline is the load-bearing variable, not utility risk.

§ 02 · STACK COMPARISONThree stacks. One winner.

Three candidate stacks ran the same 200-iteration Monte Carlo against the base scenario. The selected hybrid is not the highest-IRR option — recip-only beats it by 2.5 percentage points. The IC give-up on IRR buys three things they have explicitly named as decision-relevant: ESG narrative for the hyperscale tenant, air-permit tractability, and fuel-supply diversity.

| Stack | CapEx | LCOE | NPV (20yr · 8%) | IRR | LOLE | Verdict |

|---|---|---|---|---|---|---|

| Stack A — Recip-only (5×12.5 MW) | $78.1 M | $76.18 | +$32.4 M | 11.2% | 0.0 | Pencils, but loses on non-economic |

| Hybrid (4×12.5 recip + 30 MW solar + 15/60 BESS) | $108.5 M | $87.42 | +$11.8 M | 8.7% | 0.0 | Selected |

| Stack C — Solar-heavy (60 MW PV + 30/120 BESS) | $109.2 M | $95.30 | −$8.4 M | 6.1% | 4.2 | Fails Tier IV reliability |

Stack A loses on three non-economic dimensions: the hyperscale tenant's procurement organization has a 30% stack-renewables target on new colocation deals; air-permit precedent for 5×12.5 MW recips runs longer than for 4×12.5 MW; and single-fuel concentration is a fall-back-free posture. Stack C is disqualified — LOLE 4.2 events/year against a Tier IV target of 0.1 fails the lease's uptime test before economics even matter.

As of 2026-05-22: Wartsila quotes refreshed within 90 days, CSI Solar EPC quote binding through 2026-09, Southwest Gas LOI signed, IA executed with the rider. Outstanding: second BESS-vendor LOI in negotiation — the binding-rank-1 risk in Tier 2's Monte Carlo.

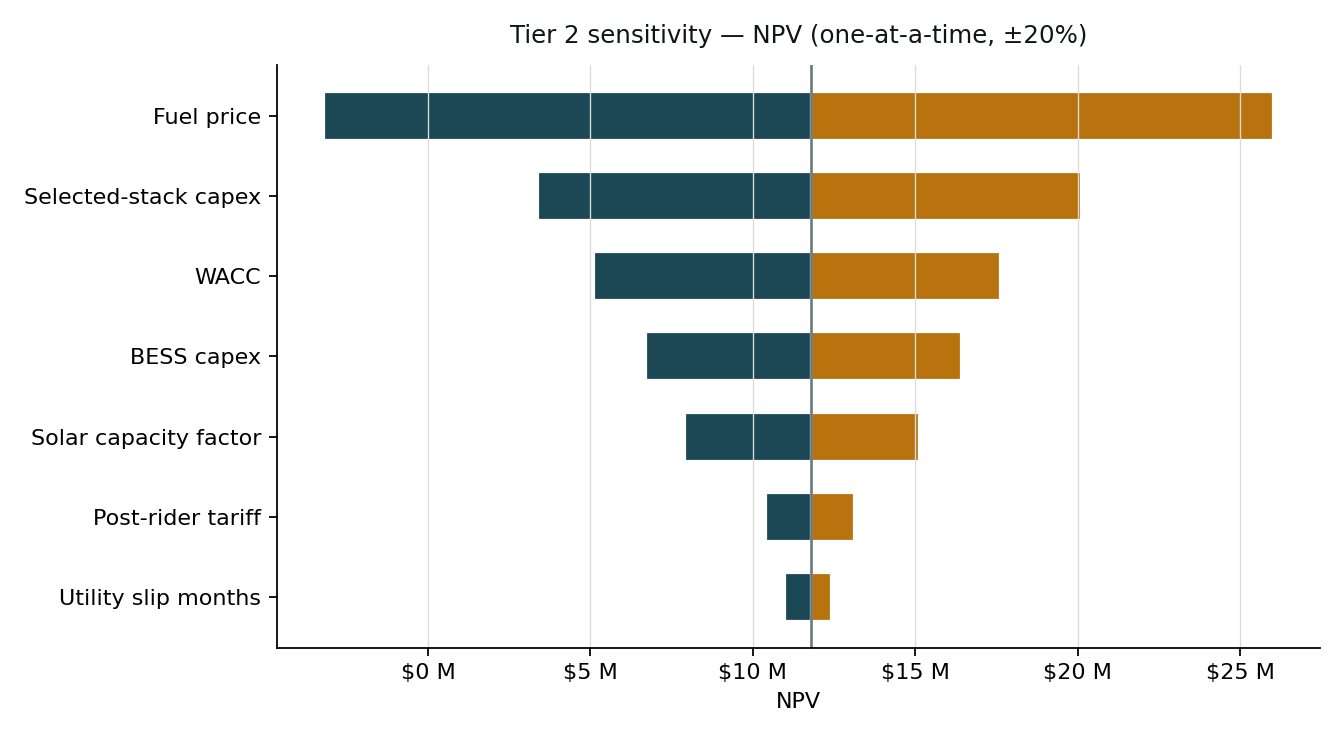

§ 03 · SENSITIVITY TORNADOWhat still moves the answer.

The Tier 1 tornado was dominated by tariff and utility-slip risk. Both have been pulled out of the random sample by the executed contracts. What's left, in order of NPV impact, is fuel price, equipment capex, and BESS capex. The operator can directly influence fuel price through firm supply terms and hedging; the others are addressable through procurement discipline.

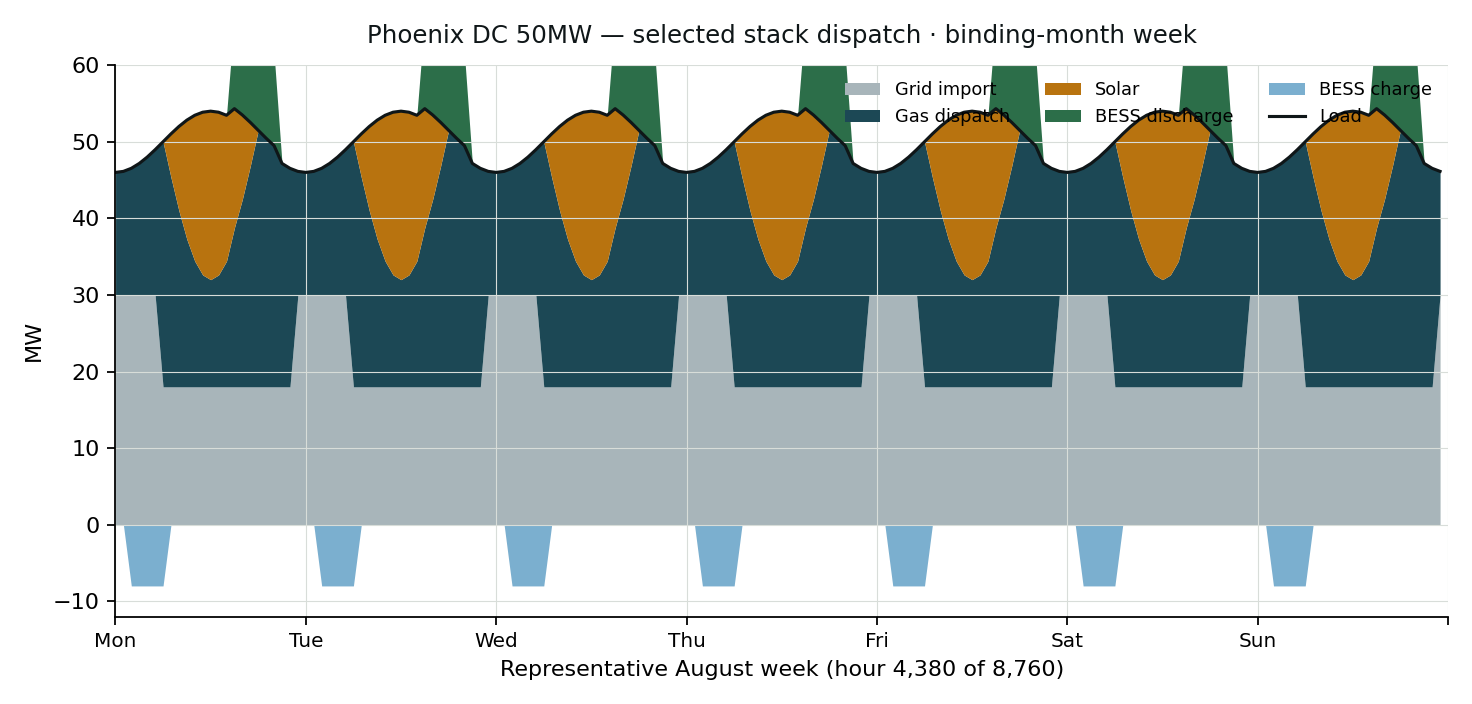

§ 04 · DISPATCH WALKThe plant during its hardest week.

August in Phoenix is the binding month — peak load (cooling) and peak demand charges (tariff structure) coincide. The dispatch walk converts the LCOE/NPV abstractions into a picture the operator's plant manager can point at: when the recip runs, when solar carries the load, when the battery covers the demand charge.

BESS pre-charging

BESS charging from solar + off-peak grid in the 02:00-06:00 window — pre-positioning for the 15:00-20:00 demand-charge avoidance.

Solar peak

Solar carries 44% of load instantaneously; gas runs at minimum stable load to avoid restart cost on cloud transients.

BESS at 12 MW · demand-charge avoidance

Each MW of BESS discharge during this window saves $20.50 / kW-month. Over 80% of BESS revenue comes from this, not from $/MWh arbitrage.

Gas at 50 MW · the binding hour

BESS depleted, sunset, full demand-charge period — the recip is the only firm asset. This is the hour that sized the gas headroom.

§ 05 · INVESTMENT COMMITTEE MEMOApprove.

Approve.

Both Tier 1 pre-feasibility actions landed on schedule. The selected hybrid stack clears the 8.0% IRR hurdle with margin (8.7% base, 7.4% under +20% fuel stress). Reliability passes Tier IV with margin. Recommend proceeding to the Tier 3 Developer Package on the 2026-06-22 target.

One outstanding gating item before construction commits: a second BESS-vendor LOI to address the rank-1 binding risk. Saguaro working it; target close 2026-06-30.

Top 5 risks (Tier 1 → Tier 2 movement)

- BESS supply chain — 28.3% binding (was 16.1%). Same exposure, not yet mitigated; relative reweighting after utility-slip risk pulled out.

- Air permit (NOx on recips) — 23.4% (was 21.7%). Pre-application meeting 2026-05-30.

- Fuel price excursion — 19.1% (NEW; was a sensitivity, now visible as a binding risk in the MC).

- Construction execution — 15.7% (was < 5%; visible now that #1 risks removed).

- Gas pipeline tap — 9.2% (was 8.4%). Southwest Gas LOI signed 2026-05-08.

The Tier 1 #1 risk (APS substation slip, 32.4%) has been mitigated by the executed APS letter and now sits at risk #11 with 1.1% binding share. That's the contractual progression the IC asked for at Tier 1.

A Tier 2 IC memo is investment-grade for the decision the IC is being asked to make. It is not a substitute for an executed offtake lease, a final EPC scope, an air-permit application, or a model handoff to the project's operating team. Tier 3 (Developer Package, 8 weeks) is the right next step on the recommended Approve; the Tier 2 bundle is its natural input.