§ 01 · GRID SHORTFALLThe grid alone leaves a 22 MW gap.

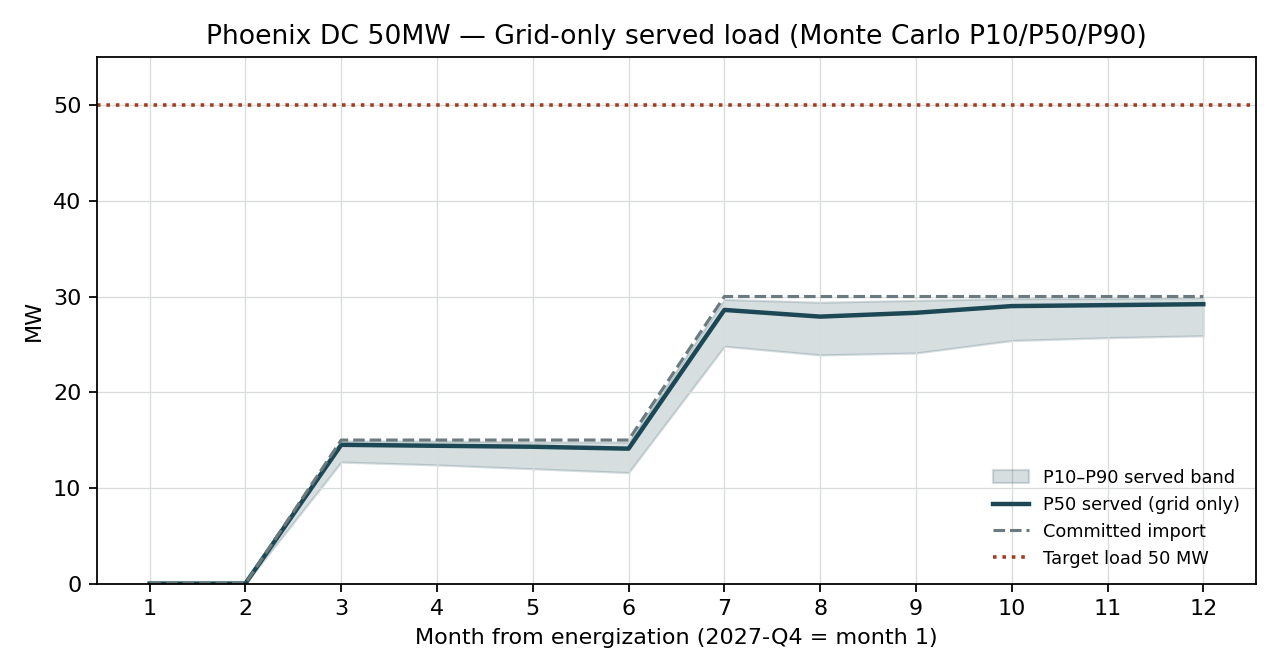

The hyperscaler tenant requires Tier-IV-equivalent service starting Q4 2027. APS has verbally committed to 30 MW near-term import, with full 50 MW deferred to Q1 2029 pending the Liberty substation rebuild. We ran 200 Monte Carlo iterations of the Layer 1 + Layer 2 model — sampling APS milestone slip, transformer and 69 kV line lead times, Phoenix weather, and equipment outages — to ask one question: can the grid carry the load through that window?

It cannot. Across the 12-month energization window, the grid alone serves an average of 27.6 MW, with a P50 worst-case of 27.9 MW in August. Months 1-2 receive zero import while interconnection completes; months 3-6 hold steady at 15 MW partial service; months 7-12 climb to the committed 30 MW. The result is a structural ~22 MW gap that any Tier-IV operation must close behind the meter.

The gap is solvable with conventional BTM technology — Phoenix has good solar resource, gas access, and supportive permitting. It is not solvable with grid renegotiation alone. The single load-bearing assumption from this section is APS's 2029-Q1 full-service date; if it slips, the BTM stack must run an additional 6-12 months and the economics change materially.

§ 02 · CANDIDATE BTM STACK50 MW firm at $108.1 M.

The recommended stack is a hybrid: 50 MW of reciprocating gas for firming and minimum-viable energization, 30 MW of solar for energy-cost reduction, and a 15 MW / 4-hour BESS for on-peak demand-charge avoidance. The 50 MW recip headroom is sized to carry the entire load during months 1-2 when grid import is zero.

| Asset | Spec | Capacity | Capex/kW | Capex (total) |

|---|---|---|---|---|

| Reciprocating gas | Wartsila 20V34SG · 4 units | 50.0 MW | $1,250 | $62.5 M |

| Solar PV | Ground-mount, single-axis tracker | 30.0 MW DC | $1,000 | $30.0 M |

| BESS | LFP · 4-hour | 15.0 MW / 60.0 MWh | $260 / kWh | $15.6 M |

| Total stack | 50.0 MW firm | $108.1 M | ||

Headline economics

Reliability is not the binding question — the stack meets Tier IV with margin. The economic story is. At base assumptions, IRR (6.6%) sits 1.4 percentage points below the client's 8% hurdle, and NPV is negative by $9.5 M against a $108 M base. Within Tier 1 noise, but flagging.

Two alternate stacks were screened. Recip-only (5×12.5 MW) pencils at $78.1 M capex and 9.4% IRR, but loses on ESG narrative for the hyperscale tenant, fuel concentration risk, and air-permit difficulty. Solar + BESS only fails Tier IV reliability with LOLE of 4.2 events/year. The hybrid wins on the non-economic dimensions, at the cost of a 2-3 percentage-point IRR vs. recip-only.

P10 (favorable supply, low EPC overhead): $96 M. P50 central: $108.1 M. P90 (BESS supply tightness, gas-engine slip): $124 M. Residual P90 unserved: 2.3 MW during BESS commissioning, addressed via short-term bridge-power rental rather than oversizing.

§ 03 · TOP 5 PROJECT RISKSRisks ranked by binding-iteration share.

A risk that "binds 32% of the time" was the worst-case constraint in 32 of every 100 simulated futures. This metric distinguishes risks that matter from risks that occur. A frequent risk that always sits inside slack is less important than a rarer risk that consumes the project when it lands.

APS substation rebuild slip

EvidenceLiberty substation work is the single milestone driving the full-service date; system-impact study still underway as of intake.

MitigationGet the 30 MW commitment in writing before IC vote. Escalate substation timeline to APS senior management. Stack sized to keep running if substation slips to 2030-Q1.

Air permit (NOx ceiling on recips)

EvidenceMaricopa County air-permit precedent for utility recips runs 9-14 months. SCR retrofit cost not yet bid.

MitigationBegin air-permit application during feasibility, not after. Price SCR retrofit in baseline. Consider lower-NOx engine option if pricing competitive.

BESS supply chain

EvidenceLFP cell allocation across hyperscaler / utility-scale demand. 2027 delivery slots already constrained as of 2026-Q1.

MitigationLOI with two BESS vendors before feasibility kickoff. Pre-order cells via deposit. Price 60 MWh and 80 MWh options.

Tariff structure change (E-36)

EvidenceAPS rate case filing expected 2027. On-peak demand charge ($20.50/kW) is a meaningful share of the savings stack. Large-load tariff design is a national 2026-2027 theme.

MitigationNegotiate fixed-rate tariff rider during interconnection-agreement signing. Engage APS regulatory affairs early. Model E-36 + 25% demand-charge case as a sensitivity.

Gas pipeline tap + interconnection

EvidenceSouthwest Gas 12" lateral 0.4 mi off-site. Tap + station design typical 12-18 months.

MitigationBegin gas-tap application in parallel with electric IA. Lock LOI for fuel supply. Price firm vs. interruptible.

The screener tracks roughly 20 risk categories. Risks below rank 5 each contribute under 5% of binding iterations and are recorded in the full register inside run-summary.json for the client's records.

§ 04 · GO / NO-GO MEMOConditional Go pending two actions.

Conditional Go for Tier 2 feasibility — pending two pre-feasibility actions.

The technical case is sound. The economic case sits 1-2 percentage points below your 8% IRR hurdle at base assumptions. Two specific actions, taken before committing the $1.8M Tier 2 spend, can close the gap:

- Get APS's 30 MW near-term import commitment in writing, with a stated full-service date for the remaining 20 MW.

- Negotiate a fixed-rate tariff rider in the Interconnection Agreement, locking the on-peak demand charge for at least 10 years.

If both actions land, base-case IRR moves to ~8.4-9.1% and the recommendation hardens to a clean Go. If either fails, the recommendation flips to defer 9-12 months until APS substation timing clarifies.

Next actions

- By 2026-05-08 — Saguaro project finance to obtain written 30 MW commitment from APS planning, including stated full-service date.

- By 2026-05-12 — Sgridworks to draft tariff-rider language for Saguaro counsel to insert into the IA.

- By 2026-05-15 (board meeting) — IC reconvenes with both pre-feasibility actions resolved; vote on Tier 2 spend.

- If both actions land — Tier 2 Power Stack Model kickoff target 2026-05-22; 6-week scope.

A Tier 1 screen is decision-grade, not investment-grade. It answers "should this project proceed to feasibility?" — not "approve this construction." The Tier 2 Power Stack Model and Tier 3 Developer Package are the right next steps if a screen recommends Go. We deliberately keep Tier 1 cheap and fast so the answer arrives before the developer commits to feasibility spend, not after.